If you’ve ever applied for coverage, you’ve probably realized life insurance companies look at more than just your age. Height and weight come up almost immediately. Many applicants quietly open a bmi calculator before filling out the form, just to see where they stand. And that leads to the bigger concern: how much does bmi affect life insurance decisions and pricing in real terms?

It’s not a small detail. Body mass index, or BMI, is one of the first screening tools used in insurance underwriting. It doesn’t tell the full story about your health, but it does influence how insurers classify risk. And risk is what determines your life insurance premiums.

How much does bmi affect life insurance when you apply?

Let’s address the core question directly: how much does bmi affect life insurance approval and cost?

In most traditional policies, BMI plays a measurable role in determining your health rating class. A higher body mass index can move you from “preferred” to “standard,” or from “standard” to a substandard rating. That shift can increase life insurance rates by hundreds sometimes thousands of dollars over the policy’s lifetime.

BMI and life insurance are closely linked because weight is statistically connected to long-term health risks such as heart disease, diabetes, and stroke. Insurers rely on actuarial tables. They aren’t judging appearance; they’re evaluating probability.

That said, BMI is only one factor among many insurance risk factors.

Why insurers use BMI in the first place

Insurance underwriting depends on data. Body mass index is easy to calculate, standardized, and widely used in medical research. It gives insurers a quick baseline.

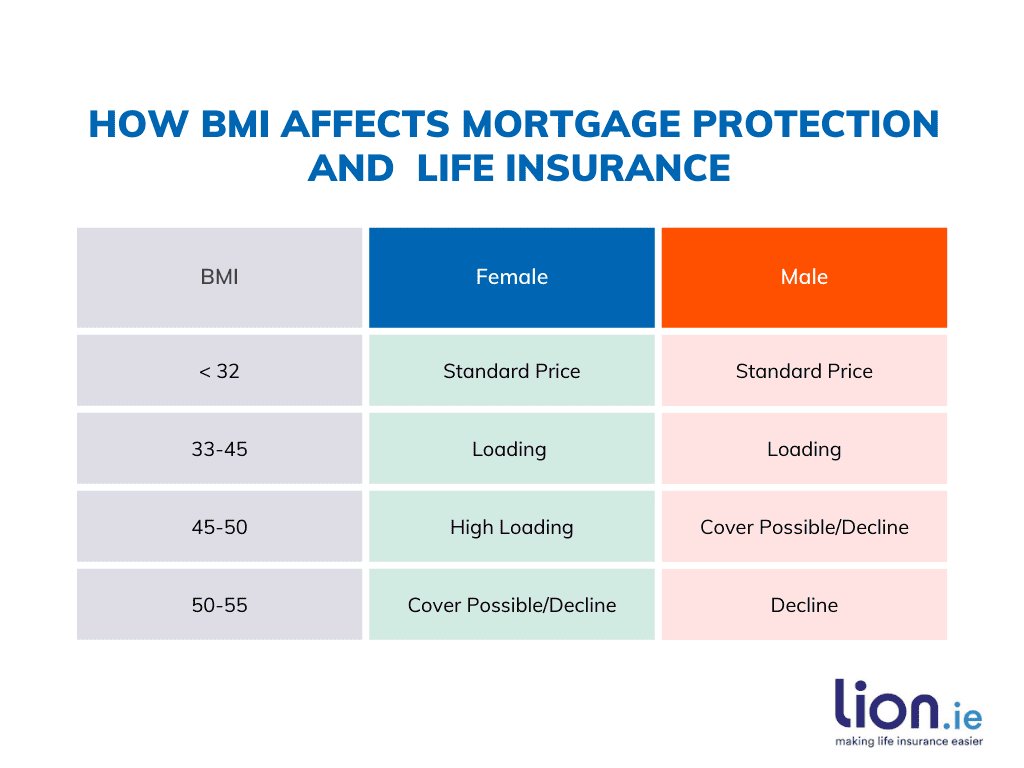

For example, here’s a simplified BMI classification chart insurers often reference:

| BMI Range | Classification | Typical Insurance View |

|---|---|---|

| 18.5 – 24.9 | Normal | Eligible for preferred rates |

| 25 – 29.9 | Overweight | Often still preferred |

| 30 – 34.9 | Obese (Class I) | Standard rates possible |

| 35 – 39.9 | Obese (Class II) | Table ratings likely |

| 40+ | Obese (Class III) | Higher premiums or decline |

The exact cutoffs vary by company. Some insurers are more flexible than others. Applicants researching bmi for women sometimes notice slightly adjusted build charts. Certain insurers account for gender differences in body composition when assigning health rating classes.

Does BMI increase life insurance premiums automatically?

Not automatically but often.

When people ask, does BMI increase life insurance premiums, they usually expect a yes or no answer. The real answer is conditional. A BMI slightly above normal may not change your rate class at all. A BMI significantly above the company’s build chart likely will.

Life insurance rates are based on tiers such as:

- Preferred Plus

- Preferred

- Standard Plus

- Standard

- Table Rated (A, B, C, etc.)

The difference between preferred vs standard rates can be substantial. A 35-year-old male applying for a $500,000 20-year term policy might see something like this:

| Health Class | Monthly Premium |

|---|---|

| Preferred Plus | $28 |

| Preferred | $34 |

| Standard | $52 |

| Table B | $78 |

A BMI shift alone can move you between these tiers.

Medical exam life insurance and weight verification

With medical exam life insurance policies, your height and weight are verified by a paramedical professional. It’s not self-reported. They measure, record, and sometimes collect blood samples.

That medical exam life insurance process gives insurers a clearer picture of cholesterol levels, blood pressure, and glucose. Sometimes an elevated BMI paired with excellent lab results softens the impact.

In contrast, no-exam policies rely on databases and health questionnaires. BMI may carry slightly more weight in those cases because there’s less detailed health information available.

How age interacts with BMI in underwriting

Age changes everything. A BMI of 32 at age 25 may be treated differently than a BMI of 32 at age 55. Insurers view long-term exposure differently depending on life stage.

People often check their biological timelines using tools like an age calculator, especially when trying to apply at the “right time.” The younger you are, the less compounded risk insurers assume. That can soften the premium impact. Older applicants may see stricter BMI requirements for life insurance approval because additional age-related insurance risk factors are present.

Timing, applications, and even geography

Application logistics sometimes matter in subtle ways. For example, insurers may process applications in centralized offices across time zones. Applicants scheduling medical exams sometimes use a timezone converter when coordinating between states.

While that doesn’t affect underwriting directly, delays between application and exam can. If weight fluctuates significantly between those dates, your recorded BMI might differ from what you expected.

Is BMI the most important health factor?

It’s important, but not the only thing. BMI and life insurance decisions are also influenced by:

- Blood pressure

- Cholesterol ratios

- Family history

- Smoking status

- Diabetes

- Lifestyle habits

Someone with a BMI of 31 but perfect blood work and no family cardiac history may receive better life insurance rates than someone with a BMI of 25 who smokes. Insurance underwriting blends all these factors together. BMI is a shortcut metric, not a final verdict.

How much does bmi affect life insurance compared to smoking?

Smoking almost always has a larger impact than BMI alone. A smoker with a “normal” body mass index will usually pay significantly more than a non-smoker with a moderately elevated BMI. Here’s a rough comparison for a 40-year-old applying for $250,000 coverage:

| Applicant Type | Estimated Monthly Premium |

|---|---|

| Non-smoker, BMI 24 | $30 |

| Non-smoker, BMI 32 | $45 |

| Smoker, BMI 24 | $95 |

That gives perspective. BMI matters, but smoking is often the heavier driver of life insurance premiums.

Build charts and technical underwriting systems

Underwriters rely on internal build charts. These charts convert height and weight into eligibility thresholds.

Interestingly, these systems operate almost like data conversion logic not unlike a number base converter translating values between formats. In underwriting software, your height and weight are input, and the system instantly maps you to a rating range. It feels mechanical because, in many ways, it is.

Can you improve your rate by losing weight?

Yes, though timing matters.

If you lose weight before applying, your BMI calculation improves instantly. If you lose weight after a policy is issued, you can sometimes request reconsideration after 12–24 months of stable improvement.

Some insurers allow re-underwriting. Others don’t. Applicants wondering how much does bmi affect life insurance often overlook this: rates are locked once approved. If you expect to improve your health soon, it may be worth waiting a few months before applying.

BMI requirements for life insurance approval

Every insurer sets its own BMI requirements for life insurance approval. Some cap eligibility at a BMI of 45. Others may decline applications above 50.

Certain companies specialize in high-BMI applicants and design policies for that demographic. That’s why shopping around matters. Two insurers may view the same body mass index differently.

Term vs whole life and BMI impact

Term life policies are more sensitive to underwriting classifications because pricing is tightly aligned with risk duration. Whole life policies may show similar BMI impacts but sometimes have slightly more flexibility depending on dividend structure and company philosophy. Still, life insurance premiums reflect health rating classes across both types.

Realistic example scenario

Consider a 38-year-old woman, 5’6”:

- At 150 lbs (BMI 24.2): Preferred rates

- At 185 lbs (BMI 29.8): Still possibly preferred

- At 210 lbs (BMI 33.9): Standard

- At 240 lbs (BMI 38.7): Table rating

That shift from preferred vs standard rates can increase lifetime cost by thousands. So when asking how much does bmi affect life insurance, the answer becomes clearer it can meaningfully shift pricing tiers.

Is BMI outdated or unfair?

Some critics argue body mass index oversimplifies health. Athletes with high muscle mass may have elevated BMI but low body fat. Insurers recognize this in some cases, especially if lab results support good metabolic health.

Still, insurers rely on decades of mortality data. Until new standardized measures replace BMI broadly, it will remain embedded in insurance underwriting.

Strategies to position yourself better

If your BMI is borderline between two rating tiers, small changes can matter.

- Maintain stable weight for at least 6 months

- Improve blood pressure readings

- Lower cholesterol

- Avoid nicotine

- Stay physically active

These improvements can offset borderline BMI concerns.

Mental stress around weight and insurance

There’s often anxiety tied to weight-based pricing. Applicants sometimes feel judged. The underwriting process is less personal than it feels. Actuarial science doesn’t evaluate character, it evaluates mortality probability. Understanding how much does bmi affect life insurance reduces uncertainty. Once you see the structure, it feels less mysterious.

When BMI matters less

Guaranteed issue life insurance policies typically do not consider BMI at all. These policies skip medical exams but charge significantly higher premiums. They’re usually last-resort options for applicants with serious medical conditions.

Final perspective

So, how much does bmi affect life insurance? It affects it enough to influence your health rating class, and your health rating class directly affects your life insurance rates. A moderate increase in body mass index might only shift you slightly. A significant increase can move you into table-rated territory. BMI and life insurance are connected, but they aren’t inseparable from the bigger health picture. Blood work, lifestyle, age, and smoking status often matter just as much sometimes more.

If you’re close to a rating threshold, small improvements can change your outcome. If not, shopping among insurers may still find a better fit. In the end, life insurance premiums reflect probability, not perfection. Body mass index is part of that equation not the entire equation.